How To Obtain A Medical Loan

By the Pachyy Editorial Team The Pachyy Editorial Team comprises a diverse and experienced team of writers, researchers and subject matter experts whose aim is to provide you with useful insights, guidance and commentary on all matters related to your personal finances.

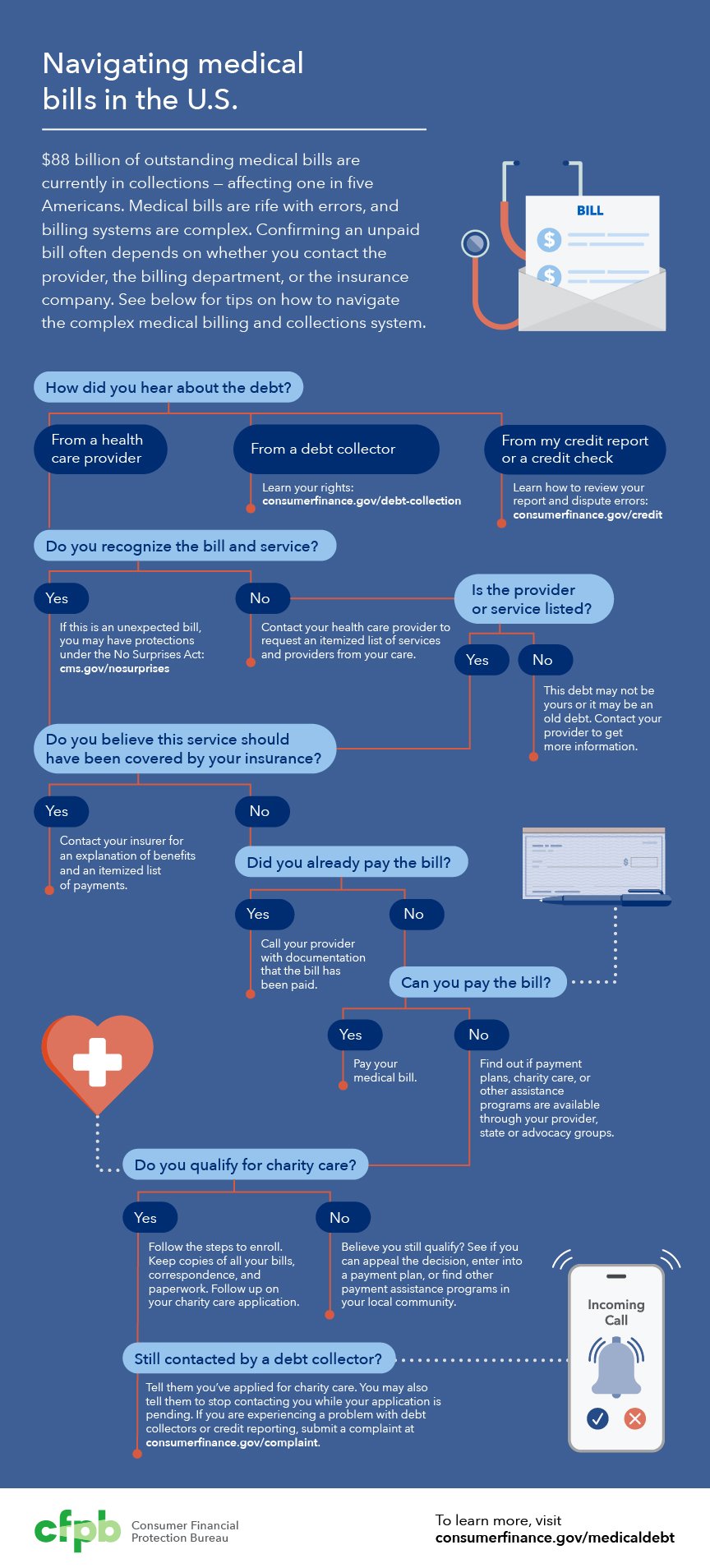

If you are facing medical debt and need assistance, there are various ways to access medical loans or find financial support through programs or personal loans. It’s important to remember that you are not alone – there are many others who are also struggling with medical bills. In fact, debt collectors have received around $88 billion in outstanding medical debts.1 According to the Consumer Financial Protection Bureau, approximately one in five Americans are currently dealing with medical debt.1 If you are finding it difficult to pay off your medical bills, it’s essential to explore options for obtaining a medical loan. On this page, you will find information on how to handle medical bills, as well as strategies to regain financial stability, allowing you to focus on your recovery. We are here to help!A Helpful Guide: How to Obtain Medical Loans

When facing accurate and legitimate medical bills, it’s important to prioritize their payment. Unpaid medical bills can negatively impact your credit score and put you at risk of collections. If you are unable to pay off your medical bill immediately, there are several options for obtaining medical loans. To ensure you choose the best medical loan for your financial situation, follow the steps outlined below.Step One: Check Your Credit Score

Your first step in finding the ideal medical loans is to assess your current credit score and review your credit report. Your financial and credit history will help determine which personal loans you are eligible for. Typically, individuals with excellent credit scores have higher chances of loan approval with lower interest rates, more flexible payback terms, and larger loan amounts. On the other hand, borrowers with bad credit may qualify for lower funding amounts and higher interest rates.Step Two: Determine Your Desired Loan Amount

The next step is to calculate the funding amount required to cover your medical expenses. Add up the balances of all your medical bills to determine your total debt. If your debt is substantial, a long-term personal loan may be more suitable. For lower balances, short-term personal loans may be a better option.Step Three: Compare Different Medical Loans

Once you have determined your funding needs, research lenders online and in your area. Compare interest rates, payback terms, funding amounts, and turnaround times for various loan products available in the market.Step Four: Find Suitable Medical Loans and Submit Your Application

The final step is to submit your personal loan application! Once you have identified a lender that seems like a good fit, fill out their online application. If approved, work with a loan agent to establish a payment plan that aligns with your personal budget. Before your approved funds are sent, your lender will present a loan agreement for you to sign. Take the time to carefully review the contract and ensure you understand all its terms. If you have any doubts or questions, don’t hesitate to seek clarification from your lender. Once you feel comfortable, sign the agreement and receive your loan proceeds.Medical Loan Applications

Try to limit the number of medical loan applications you submit to just one or two lenders. Each time you apply for a loan, it results in a hard credit inquiry on your profile. Having too many hard credit inquiries within a short period may raise concerns for lenders and make them hesitant to work with you in the future.What Is a Medical Loan?

A medical loan is a type of loan that you can use to pay for your medical expenses. Whether you need to cover the costs of a planned procedure or have an unexpected trip to the emergency room, a medical loan can help you manage these expenses. You have various options for applying for a medical loan:- Online providers

- Direct lenders

- Credit unions

- Bad credit lenders

- Banks

Helpful Tips for Dealing with Medical Bills

Dealing with medical bills can sometimes be overwhelming, but don’t worry! Here are some friendly and useful tips to navigate through the process. When you receive a medical bill, take the time to carefully review it to make sure everything is correct. Start by checking the sender. If it’s from your healthcare provider, consider requesting an itemized receipt. This will help you better understand the costs and identify any charges that may seem unfamiliar to you. Don’t hesitate to ask for clarification if something doesn’t make sense. It’s possible that certain charges are there by mistake. If you receive a bill from your healthcare provider unexpectedly, you may be covered under the No Surprises Act. This can provide you with additional protections and rights. Now, if the bill comes from a debt collector, it’s important to know your rights. Starting from November 30, 2021, the Debt Collection Rule dictates how and when debt collectors can communicate with consumers. As part of this rule, debt collectors are required to disclose information about the account creditor and any associated account numbers. If you don’t see this information on the bill, it’s possible that the debt collector made an error. In such cases, feel free to dispute the incorrect medical collections to avoid any negative impact on your credit report. Remember, you have the right to understand and question your medical bills. By taking these steps, you can handle them effectively and protect your financial well-being.How to Choose the Right Loan for Your Medical Expenses

| Criteria | Description | Tips |

| Eligibility | Criteria set by lenders to qualify for a loan. | Check lender-specific requirements like employment status, income level, and residency. |

| Loan Term | Duration over which the loan is repaid. | Longer terms mean smaller monthly payments but more interest over time; shorter terms are the opposite. |

| Fees | Additional charges associated with the loan. | Look out for origination fees, late payment fees, and prepayment penalties. |

| Interest Type | Fixed vs. variable interest rates. | Fixed rates stay the same throughout the loan term, while variable rates can fluctuate. |

| Application Process | Steps to apply for a medical loan. | Typically involves an online application, document submission, and possibly a credit check. |

| Co-signer Option | Involving another person as a guarantor. | A co-signer with a good credit score can improve approval chances and possibly secure better terms. |

| Loan Use Restrictions | Limitations on how loan funds can be used. | Ensure the loan can cover all intended medical expenses, including aftercare or related costs. |

| Customer Support | Assistance provided by the lender. | Consider lenders with strong customer support for guidance and help during the loan term. |

Interest Rates

One of the most important details of a loan is the interest rates. Your interest rate will determine how long it will take to pay off your personal loan, as well as how much the loan will cost overall. As discussed, borrowers with a better credit score are more likely to receive lower rates. If you are trying to boost your credit score in order to receive better interest rates, you can try the following:- Work on your payment history.

- Pay off outstanding debts.

- Limit the number of credit applications you submit.

Origination Fees and Other Costs

During your loan research, check to see which lenders require origination fees or other costs. An origination fee is a charge implemented by some lenders when borrowers sign their loan contracts. Borrowers can usually choose to pay their origination fee upfront or have the charge added to their total loan balance. Some lenders charge no origination fees at all.Repayment Terms

Another important aspect of your personal loan to consider is the repayment terms. The longer you take to pay back a loan, the more you will end up paying out of pocket in interest fees and other charges. To pay off your balance faster, try to pay more than the minimum monthly payment on your medical loan.Explore Alternatives to Medical Loans

Before you rush into applying for a medical loan, let’s consider some alternative options that may be more beneficial for you.Check Your Health Insurance Coverage

Before dipping into your own savings for medical expenses, reach out to your healthcare provider and inquire about your health insurance coverage. In many cases, health insurance can cover a significant portion, if not the entire cost of your medical procedure or emergency room visit.Investigate Financial Assistance Programs

Depending on your financial situation, you might qualify for government medical financing assistance. Explore programs like Medicaid and CHIP, which offer support for both adult and child medical expenses.Consider Medical Payment Plans

Engage in a conversation with your medical provider to explore the various medical payment plans they have available. These plans enable you to divide your total balance into manageable monthly payments. This arrangement can alleviate the anxiety of a large debt and helps you avoid unnecessary interest rate fees that come with traditional personal loans.Explore Medical Credit Cards

An alternative to medical loans is obtaining a medical credit card. CareCredit is a reputable provider offering these cards that are accepted by over 250,000 providers nationwide. These medical credit cards can be used for a range of procedures such as LASIK, vision care, dermatology, dentistry, certain veterinary procedures, and hearing care. Payments made with a medical credit card directly go to your medical provider. Additionally, using a medical credit card may offer lower interest rates and more favorable payback terms than traditional credit cards.Consolidate Your Medical Bills

If you find yourself juggling multiple outstanding medical bills, it might be wise to consolidate your debts through a personal loan. Instead of dealing with various payments, consolidating allows you to make a single payment to cover all your medical expenses. Be cautious, though, to avoid predatory loan options like fast payday loans, as these can lead to even more debt.Frequently Asked Questions: Paying Medical Debt

If you’re wondering how to pay off medical debt, we’re here to help! Take a look at some common questions and answers: 1. What is the minimum credit score required for medical loans? Many lenders may require a minimum credit score to approve a medical loan. While the exact score can vary, there are options accessible to individuals with fair credit. It’s best to check with specific online lenders for their specific requirements. 2. Can I get a medical loan with a fair or bad credit score? Yes! It is possible to obtain medical loans with a fair or bad credit score. Some online lenders specialize in offering personal loans to individuals with less-than-perfect credit. However, be prepared for potentially higher interest rates and different loan terms. 3. How do loan amounts vary for medical loans based on credit score? Loan amounts for medical loans can vary significantly based on your credit score. Generally, a higher credit score may qualify you for larger loan amounts at better terms, while a lower score might limit the amount you can borrow. 4. Are there any benefits to repaying medical loans early? Repaying a loan early can save you money on interest and potentially improve your credit score. However, it’s important to check if your loan agreement includes any prepayment penalties. Most lenders allow early repayment, but it’s always best to confirm. 5. What should I consider when choosing an online lender for a medical loan? When selecting an online lender for a medical loan, consider factors like interest rates, loan amounts, fees, the lender’s reputation, and customer service. Also, review the terms to ensure they align with your ability to repay and your financial situation. 6. How do personal loans to finance medical expenses differ from other types of personal loans? Personal loans for medical expenses are specifically intended to finance medical-related costs. They may offer different terms or special conditions compared to general personal loans, such as deferred payments or specific repayment plans tailored for medical expenses. 7. Can I use medical loans for any type of medical expense? Generally, medical loans can be used for a wide range of medical expenses, including surgeries, treatments, medical equipment, and sometimes even related travel costs. However, it’s important to verify with the lender if there are any restrictions on the use of the loan. 8. What are the typical interest rates for medical loans with fair credit? Interest rates for medical loans can vary widely, especially for those with fair credit. Rates are often higher than for those with an excellent credit score, but can still be competitive. It’s crucial to compare offers from multiple lenders to find the most favorable rate. 9. How quickly can I receive funds from a medical loan? The speed of funding for medical loans can vary among lenders. Some lenders may offer quick processing and disburse funds within a few business days, while others might take longer. If timing is crucial, look for lenders known for fast funding. 10. Is it possible to refinance a medical loan? Yes, refinancing medical loans is possible, especially if your credit score has improved since you took out the original loan. Refinancing can potentially lower your interest rate and reduce monthly payments. However, it’s important to weigh the costs of refinancing against the potential savings.Welcome to Pachyy’s Guide on Medical Loans!

We understand that dealing with medical expenses can be overwhelming, especially during your recovery. But don’t worry, we’re here to help! Take a look at our trusted resources for all your questions about medical loans, installment loans, interest rates, and finding affordable funding. If you’re also interested in personal loan options, you’ve come to the right place. Since 2018, borrowers have been relying on Pachyy for great deals on personal loans. With Pachyy personal loans, you can enjoy benefits such as competitive rates, quick funding*, flexible payments, and an easy application process. Ready to see how much funding you could get with a personal loan? Head over to the Pachyy application today! References:- Medical debt | Consumer Financial Protection Bureau

- Understand how the CFPB’s Debt Collection Rule impacts you | Consumer Financial Protection Bureau

- CareCredit vs General Purpose Credit Cards | CareCredit

- Help with Bills | USAGov

- Navigating Medical Bills in the US | Consumer Financial Protection Bureau

{kind=link}